View release as a PDF

Manchester—Taxpayers United of America (TUA) today released the results of a new pension study for the cities of Manchester, Concord, and Nashua; the counties of Merrimack and Hillsborough; and New Hampshire State government retirees.

“New Hampshire lawmakers have only flirted with reforms of the government pension system,” stated Jim Tobin, president of TUA. “New Hampshire has one of the lowest funded ratios in the country and reforms are still in the discussion stage.”

“While residents across New Hampshire face crushing tax increases, falling home values, rising unemployment, and a painfully slow economic recovery, government employees continue to receive stunning pensions largely funded by taxpayers who will never collect more than about $22,000 a year from Social Security.”

“New Hampshire is the 19th state in our nationwide pension reform tour and the results are consistent with our findings across the country: government pensions are out of control. Across the country, millions of bureaucrats are being paid billions, to do absolutely nothing!”

“The purpose of our study is to put some perspective around individual pensions, to put them in terms to which the average taxpayer can relate. Taxpayers need to know how much New Hampshire’s government retirees are being paid not to work and the astronomical accumulation of those payments over an average lifetime. Hundreds of government retirees’ pensions being released today will accumulate to millions of dollars in payouts.”

Tobin continued, “For example, Stephen Tierney, retired from the Manchester municipal government and collects an annual pension of $103,600. His estimated lifetime pension payout is a stunning $2,590,011.*”

“Roger C. Brooks, retired from the Concord government schools, has an annual pension of $91,746, with a staggering estimated lifetime payout of $2,293,659.* ”

“Retired Nashua municipal government employee, Michael P. Buxton, has a lifetime estimated pension payout of $4,278,910*, with an annual pension of $109,716.”

View pension amounts below:

- Concord NH Fire & Police Top 25

- Concord NH Government Schools Top 25

- Concord NH Municipal Top 25

- Manchester NH Fire & Police Top 25

- Manchester NH Government Schools Top 25

- Manchester NH Municipal Top 25

- Nashua NH Government Schools Top 25

- Nashua NH Municipal Top 25

- Nashua NH Police & Fire Top 25

- New Hampshire Judges Top Pensions

- New Hampshire State Government Top 25

- New Hampshire State Police Top 25

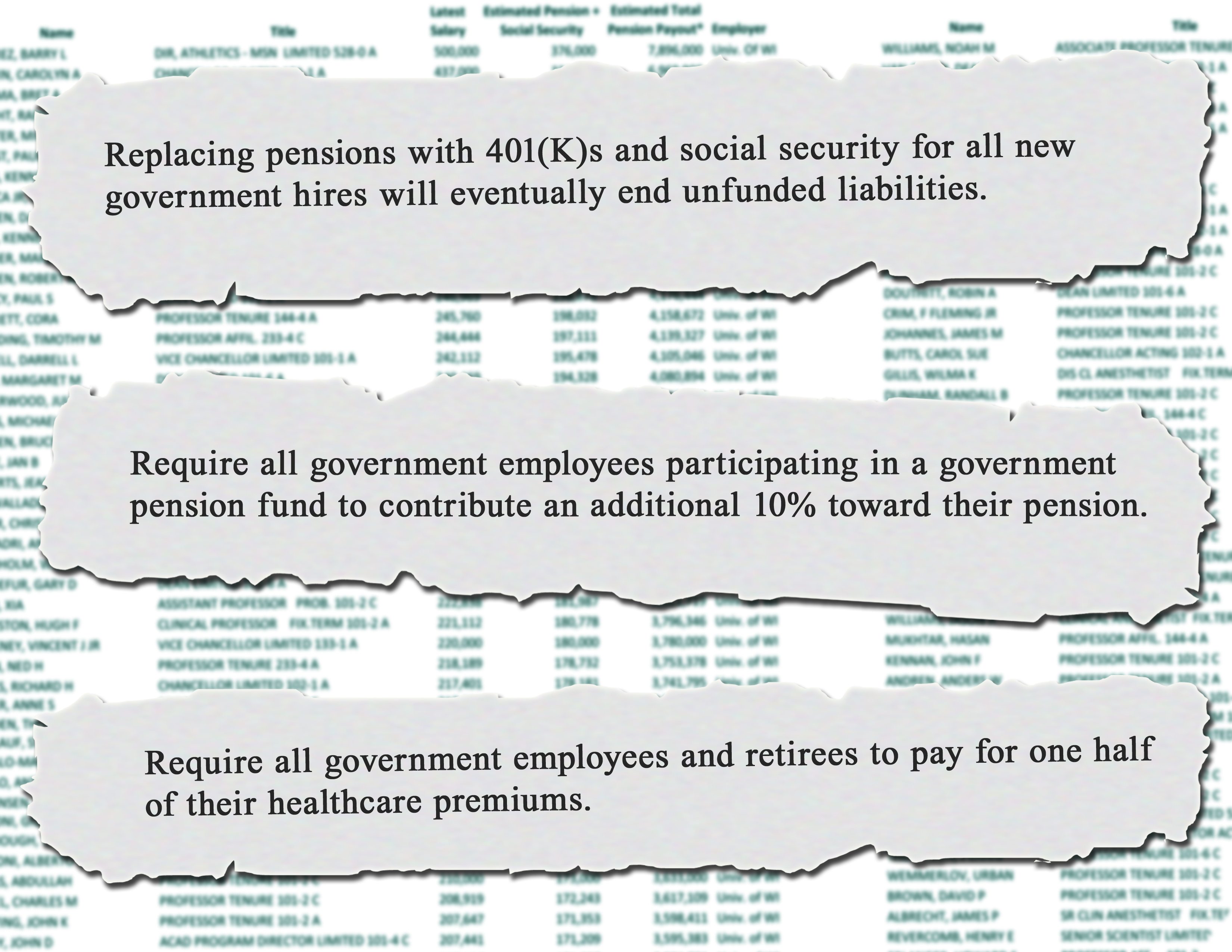

“New Hampshire’s government pensions are in serious trouble with no end in sight. Government employees should be paid a fair wage for the work they do today so they can save for their own retirement. Replacing defined benefit pensions for all new government hires with social security and 401(k)s would eventually eliminate unfunded government pensions. Current government employees must consider a voluntary pension contribution of up to 10% to preserve their pension benefits and the retirement age must be raised. Without such reforms, the system will collapse and pensions checks will simply stop coming,” added Tobin.

*Annual pensions are actual amounts provided by the respective fund. Lifetime estimates assume retirement at 60 for non-police and fire and retirement at 45 for police and fire. Uses a life expectancy of 85 (IRS Form 590).

{kind=link}

The New Hampshire taxpayer is getting ripped off! Wake up New Hampshire.

NH and other states can legally adjust the rates of the pensions. They should cap overall pension payouts to $65,000 for individuals. Some people are gaming the system by double collecting from a deceased spouse. But there shouldn’t be a penalty for marriage, thus individual and not a household cap.

That alone would be a good first step. Privatizing has mixed success. It’s premised on good outcomes in the stock market and is legally questionable. I know as a recent college grad, I’ll get virtually nothing in government-backed retirement payments (SS or pension).

An individual at retirement age has far less of a need for a bloated income than a young family of four buying a new home.

And if we’re concerned about revenues, just legalize and tax recreational drugs. If someone kills themselves with it … that’s their choice. This is supposed to be the Live Free or Die state. Mass residents have more freedom on the marijuana question.

I find the math used by the author of the article to be a bit skewed. He makes an assumption that the individual is receiving the amount quoted for the period of his computation to arrive at his seven figure amount. This is, however, not the case since most start out at a much lower number and it goes up thru cost of living increases. The COL have amounted to very little for the last several years in any case.

The author also does not take into account that those of us who work in public safety do so for less money than much of the private sector, for longer hours, holidays and at greater danger. We do this because most feel a calling to public service, to protect and serve to quote the LAPD motto. We miss birthdays, Christmas with family and other important events that most people don’t. We see the worst that society has to offer, and on occasion give up our lives to protect others. The reward for this is the hope of making it to a decent retirement and a life more normal than the previous 20-25 years. Yet when we get there we have to listen to all those who would not want to do the job of police and fire, yet begrudge what we have earned and paid for. It is a sad testimony to what society has become.

There was no COLA (Cost of Living Adjustment) used in the calculation of the estimated lifetime payouts on this study. Government employees are paid more than private sector employees, 35 percent higher wages and nearly 69 percent greater benefits according to the Bureau of Labor Statistics. They also enjoy nearly ironclad job security.

While pension reform is needed everywhere, the boilerplate quote is just wrong.

“While residents across New Hampshire face crushing tax increases,…”

no- still no income tax or sales tax

“…falling home values,…”

no- home prices are up double digits off the financial crisis

“…rising unemployment,…”

no- NH has rising employment and the lowest unemployment in the northeast

“…and a painfully slow economic recovery,…”

yes- agreed

One other point on the tax/home price issue, in most NH communities, the town and school budget is voted on by residents, so you are somewhat more in control of real estate taxes. When our valuation went down, so did our taxes.

New Hampshire home prices are down 3% from February 2011 to February 2012 and have fallen in both of the first two quarters of 2012. While NH enjoyed declining unemployment rates from June of 2009 to April of 2012, in more recent months, NH’s rate is climbing again and is now back to the Dec 2010 rate of 5.7%. New Hampshire has one of the worst pension systems in the country, in terms of unfunded liabilities. New Hampshire residents FACE crushing tax burdens if bureaucrats choose to tax their way out of this problem.

This is the myth. When valuations go down, taxes no longer go down. The town managers are so powerful now along with the school supporters that they find more things to spend money on. Registering you car is called a fee. It is a property tax everywhere else.

Robert Libbey was kind when he said the math was a bit skewed. You formulate your numbers based on an individual walking away at 45. While this may happen it often times does not. I think you will find people are more in the 50s age range when they leave. You also automaticlly use 85 at the other end for your figures. Again this is possible howeve it is not the rule. In fact I do not come across alot of 85 year old retired police and firemen.

I realize you are obviously trying to raise the hysteria level but lets take a moment and do a little research.

1. What did these individuals make when they took the job? If it was such a great deal how come more people did not hop on board?

2. How many years of service did these members work? What is the average private sector pension for a job of comparable responsibility?

3. What is the average pension of members in this system? What is the lowest 25 pension earners?

I look forward to seeing your info.

Thanks,

A concerned taxpaying NH resident.

Steve, The math is not skewed in any way. Safety officers are eligible to retire at 45 and the average life expectancy is 85. Safety officers have, according to CALPERS, the same life expectancy as non-safety officers. Why wouldn’t they? They can retire at 45, get premium healthcare and often get cost of living increases!

Your questions are outside the scope of the study or information available regarding these retired individuals. Personal information is not released and information regarding employment is not stored in the retirement fund system. Average pensions are not relevant as they include part-time and not fully vested pensioners. What is relevant, is that government employees make higher wages than private sector employees and enjoy golden benefit packages not seen in any private sector jobs.

The pension system is not sustainable. It is mathematically impossible to pay people NOT to work for more years than they are paid to work. For those that retire early, you could be paying three different people for the same single job at a given time.

Susan Forey, NH State police, retired at age 45 with a pension of $86,000.00. He last year salary was $101,000 and in 2009, $129,000.00. She had a SP car (SP3) and all expenses paid by NH taxpayers. She spent her adminstrative years at SP warming her butt on a chair.

Her husband, Rodney Forey, retired at age 45 with a pension of $54,000.00 not including his pension from the US Coast Guard. And, IMHO, he did nothing in his career.

With their pensions they get one of the best paid for medical care in the US. And they get to work in the private sector.

the problem of high pensions is with all of the uniformed state police and local administrators. The third highest state police admin retired a few years ago. She made $101,000.00 her final year by bumping her last three years with “other” pay, accumulate overtime and holiday pay from years past. she was in her mid 40’s. Her first year of retirement she was paid $86,000.00 plus benefits. Her husband also retired with a state pension of $56,000.00 plus benefits. he also gets a military pension. If they both live to be 85 they will have sucked more than twice what they were paid for 20 years. This is a very broken system.