View release as a PDF

CARSON CITY—Taxpayers United of America (TUA) today released estimated pension payouts for Carson City area and Nevada government employees. Nevada refuses to release actual government pensions, ignoring citizens’ right to review all payments funded by taxes. TUA calculated estimated pensions for government employees based on actual salaries of current government employees to shed light on the largess of the tightly guarded secret payouts.

“Nevada lawmakers and administrators are complicit in the corrupt system that allows money to be forced from the rank and file and given to politicians in the form of campaign contributions,” stated Rae Ann McNeilly, Director of Outreach for TUA.

“But it seems that some government officials are willing to protect the system by keeping it hidden from review. The costs of shielding the system from review, and ultimately, reform, are devastatingly high as cities around the country are buckling under the weight of their unfunded liabilities. Pension funds are the number one budgetary problem in the country.”

“While residents across Nevada face crushing taxes, falling home values, and double digit unemployment, and, at least according to some, another recession, government employees continue to receive lavish pensions funded by taxpayers who will never collect more than about $22,000 a year from Social Security.”

“Nevada has the highest pensions of the 14 states in which we have completed our pension studies, and yet it also suffers the highest unemployment rates and has been hardest hit by the housing crisis which is now facing a second round of foreclosures.”

“Heath Morrison, a Washoe County government school district superintendent, has an estimated annual pension of $199,548*, based on his actual annual gross of $259,153, with an estimated lifetime payout of $9,494,494.* ”

“Washoe County Medical Examiner, Ellen G. I. Clark, has a lifetime estimated payout of $8,368,037* with an estimated annual pension of $175,873*, based on her actual annual gross of $228,406.”

View pension amounts below:

- Carson City/County Gov. Employees Top 100

- Reno Gov. Employees Top 100

- Sparks Gov. Employees Top 100

- Nevada State Gov. Employees Top 100

- Washoe County Gov. Employees Top 100

- Washoe County Gov. Schools Top 100

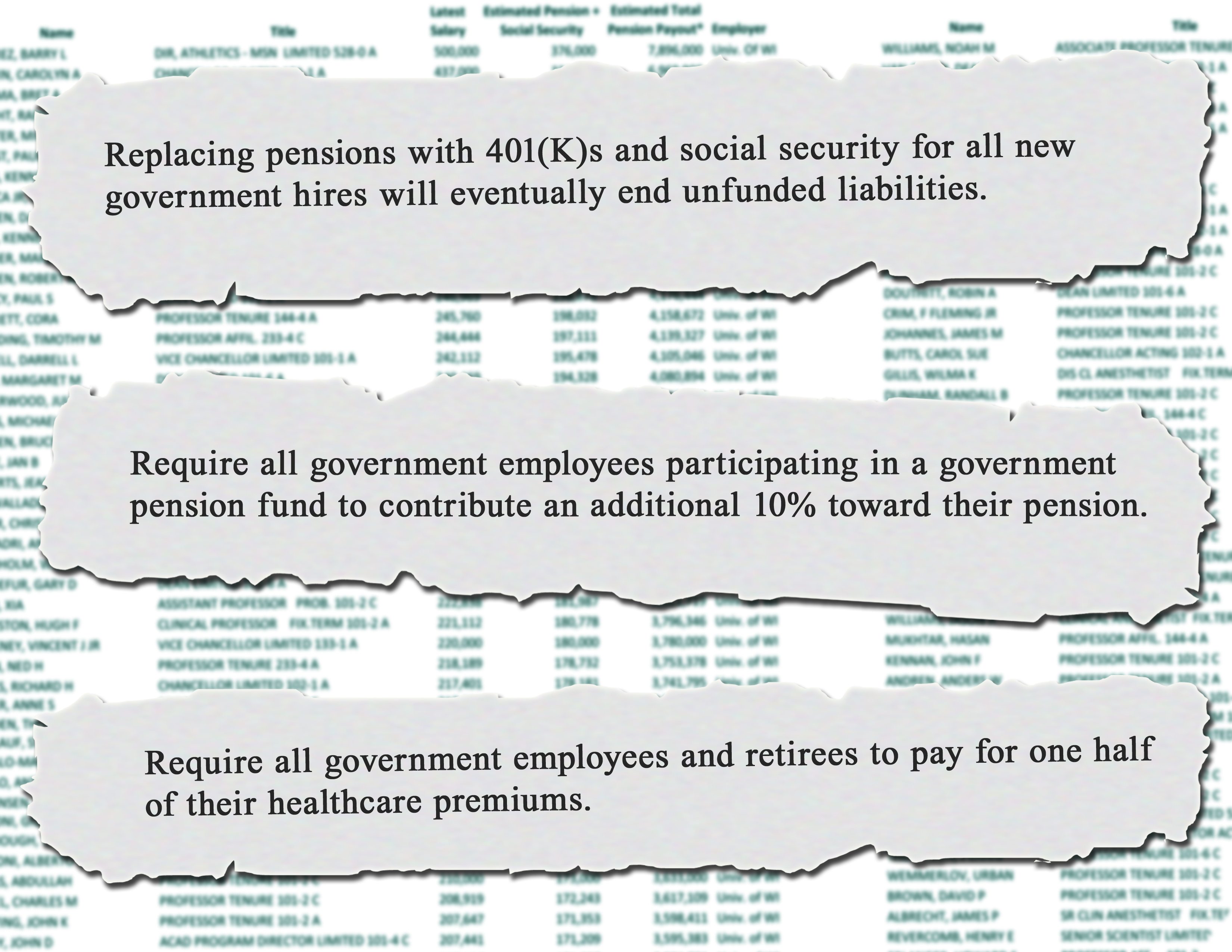

“Nevada’s government pension systems are crushing middle class Nevadans. Replacing defined benefit pensions for all new government hires with social security and 401(k)s would eventually eliminate unfunded government pensions. Current government employees must increase their pension contributions to preserve their pension benefits and the retirement age needs to be raised to at least 67. Additionally, all members should pay for 50% of their healthcare premiums. We need a stable system that is fair to both taxpayers and beneficiaries or pension checks will stop coming,” added McNeilly.

*TUA submits FOIA requests for current employee salaries and estimates pensions based on the current pension laws. COLA 2.5% per year worked, after 2001 2.67%. New employees after 2010 only 2.5%. Assumptions: 30 years age 55 (age 60 for University Employees), 77% payout, COLA avg 3%. COLA is officially none for 3 years, 2% 4,5,6 then3% 7,8,9 then 3.5% 10,11,12 then 4% 13,14 then 5% after. However there is an adjustment made if the retirement at any given year exceeds what the accumulated CPI would be for the years retired so 3% as an average has been used. Maximum 90% if they started before 1985, 75% after 1985.

{kind=link}

But don’t the employees pay for their own retirement? How can this be “crushing” for the taxpayers? The retirement program was changed so that employees were given proportionately less in wages so that their contributions wouldn’t be taxed as salary. Technically there is no longer a match from the taxpayers at all and all of the monies are donated by the employee to their retirement. It’s the employees money.