James A. DeLeo is the very model of a modern IL. politician. He was a former Democratic member of the Illinois House of Representatives, and the Illinois Senate. He was also an Assistant Majority Leader for a period.

During his time in Illinois politics, DeLeo, like so many other politicians was hostile to taxpayers. Take for example his performance in the 93rd Illinois General Assembly. He voted in favor of SB1725, a new death tax that at the time was estimated to cost taxpayers $200 million in 2004, and $500 million every year after. He voted in favor of SB842, a $59 million heavy machinery tax that targeted Illinois manufacturers, including of all things graphic design companies. He also voted in favor of SB83, a bill that allowed park districts to raise property taxes $10.5 million a year without referendum. When then Governor Blagojevich vetoed the bill, DeLeo voted in favor of the veto override.

Also like so many others, DeLeo is also a pension millionaire. DeLeo receives from his General Assembly Retirement System (GARS) pension an estimated $116,241 a year, with the majority of the money sourced from state taxpayers. DeLeo put $169,550 into his pension, and since his retirement from politics has been given an estimated $1,034,749. By the time he reaches 85, DeLeo is estimated to receive $3,377,802 from his pension.

There are plenty of pension millionaires, and we at Taxpayers United of America are going to put a spotlight on all of them! If taxpayers would like to view the latest annual report on Illinois pensions, there is a link to it on our website: 15th Annual Illinois Pension Report – Taxpayers United Of America

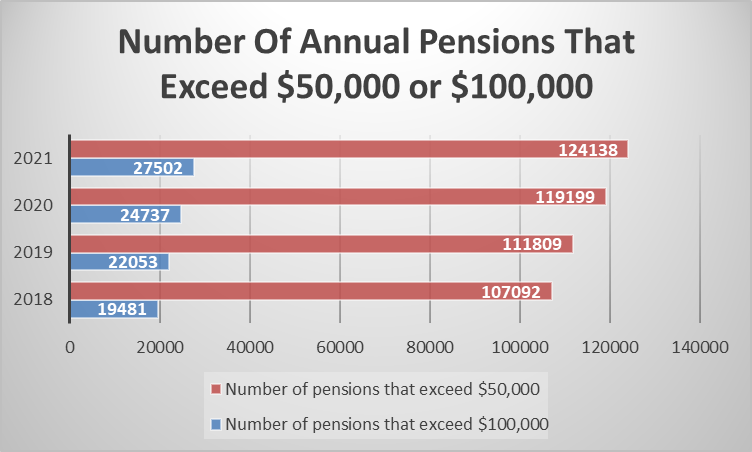

Click Here to view Pension Report Overview Last year, Illinois taxpayers were funding million-dollar pension payouts for 148,654 retired government employees. That number for our 15th annual pension study has since climbed to 151,391. These pensions are not small. According to information provided by the pension funds, 124,138 of these pensions meet or exceed an annual payout of $50,000. 27,502 of these pensions also exceed $100,000 annually. This is because the vast majority of Illinois government pensions are subject to a 3% compounded cost of living adjustment. This compounding is the primary reason we have so many pensions turning retired government employees into pension millionaires.

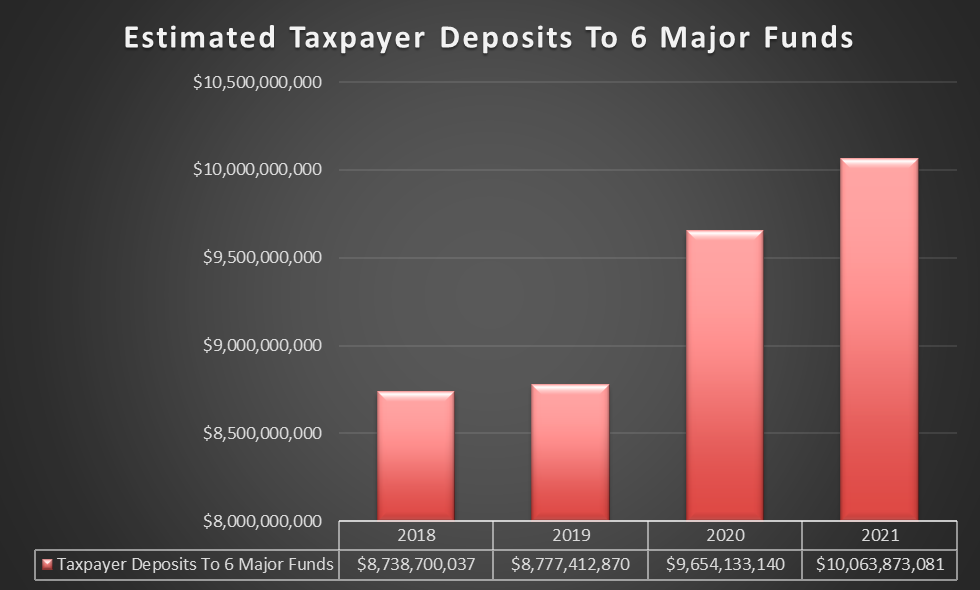

The exponential growth of the six statewide Illinois government pension funds continues unabated. These six funds include the General Assembly Retirement System (GARS), Judges Retirement System (JRS), State University Retirement System (SURS), State Employees Retirement System (SERS), Teachers Retirement System (TRS), and the Illinois Municipal Retirement Fund(IMRF). Some of the key statistics regarding how the pension system is funded are as follows:

•Taxpayers are estimated to contribute for 2021 ten billion dollars in order to fund the retirement of government employees. This is a one point three billion dollar increase from 2018.

•Taxpayer contributions are still steadily ramping upwards year over year, despite the recession.

•For the year 2021, estimated employee contributions to their own pensions are down an estimated $35 million from last year.

•The reported net position of the six state wide funds worsened another $4 billion from last year.

Some of the key statistics regarding how the pension system is funded are as follows:

•Taxpayers are estimated to contribute for 2021 ten billion dollars in order to fund the retirement of government employees. This is a one point three billion dollar increase from 2018.

•Taxpayer contributions are still steadily ramping upwards year over year, despite the recession.

•For the year 2021, estimated employee contributions to their own pensions are down an estimated $35 million from last year.

•The reported net position of the six state wide funds worsened another $4 billion from last year.

It is important to remember that taxpayer payments happen regardless of the state budget condition. While taxpayers are losing their jobs and the state coffers run dry during the pandemic, retired state employees retain an iron grip on taxpayers’ wallets. Taxpayers are also the primary source of funding for these massive pensions.

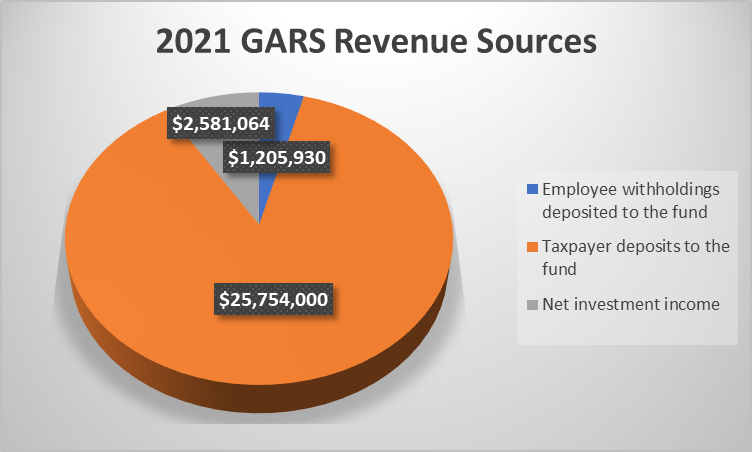

There is a wide spread narrative that the pensions are largely funded by both employee deposits and robust returns on investment. The facts, don’t bear that out. While the state of each individual pension fund is different, some like the General Assembly Retirement System refute any notion of self-reliance. For every dollar from either politicians or investments, taxpayers added an estimated $6.80 to the General Assembly Retirement System. Taxpayers pay more, and will continue to pay more into this broken system for the foreseeable future.

With the current funding requirements, all but the IMRF funding falls extremely short of necessary levels to pay every promised government employee pension.

TRS 40.5%

JRS 37.9%

GARS 16.5%

SERS 38.7%

SURS 42.2%

IMRF 90%

Although the IMRF funding level is in the proper range for a viable schedule of amortization, it doesn’t illustrate the extreme burden that this places on property owners. Illinois statute requires that IMRF pension deposits be paid by taxpayers before any other liabilities.. Under these extremes, taxpayers are being forced out of their homes because they can’t afford IMRF driven property taxes and housing expenses. Additionally, this requirement forces local governments to sacrifice services needed today in order to pay for services rendered in years past.

TEF has and does advocate for pension reforms, included but not limited to: Place all new government hires into a defined contribution account as opposed to the current defined benefit system. Immediately discontinue the automatic cost of living adjustment and make promises to only increase cost of living in alignment with current financial conditions. Remove all of the loopholes that allow salary spiking during the last years of employment on which pension calculations are made.

“Joe Biden (D) is the proverbial crazy uncle families keep in the attic, away from view. Now he has been unleashed by the Democrat Party as the presumptive presidential candidate, and his economic agenda is truly frightening,” said Jim Tobin, economist and president of Taxpayers United of America (TUA).

“Uncle Joe may not always know what planet he is on, but he knows where the money is, and he plans to assail the hard-earned capital of workers and corporations, including small businesses that are hanging on by a thread during this punishing coronavirus lockdown.”

“Biden has released his so-called Buy America Plan, which in fact is a scheme to raise taxes by almost $4 trillion, according to Issue #69 of the Committee to Unleash Prosperity.”

“According to the report, ‘No tax agenda in modern history would do more to chase jobs and investment out of the United States than this sock it to the rich sophistry. It reverses virtually every tax cut under the Trump law, which gave us the lowest unemployment rate and highest income gains in 30 years, a surge in wealth and stock values, and attracted nearly $1 trillion of foreign capital to the United States.’ Biden’s plan would erase forty years of pro-growth progress in reducing tax rates.”

The report states that “Instead of lowering rates and eliminating tax loopholes, it raises tax rates to above 50% while carving out massive new tax loopholes (for example for green energy) for favored industries of Biden’s friends and financial supporters. It is a tax plan that will make tax accountants and Washington lobbyists rich.”

Biden’s new buddy, socialist Bernie Sanders, helped write the plan, calling it “most progressive tax plan since FDR.”

“Actually it’s worse than that,” said Tobin. “Let’s speak plain English and call Biden for what he is: not a ‘moderate’ but a left-wing fool whose strings are being pulled by the most radical wing of the Democrat Party.”

Taxpayers United Of America: (TUA). is a nonpartisan, 501(c)(4) taxpayer advocacy group. Founded June 27, 1976 in Chicago, Illinois by activist and economist Jim Tobin, TUA works on behalf of taxpayers to reduce local, state, and federal taxes. In the past forty years, TUA has saved taxpayers more than $200 billion n taxes and has become one of the largest taxpayer organizations in America. Check All posts.

s.

ADDRESS

Chicago, IL 60606

205 W. Randolph Street, Suite 1305

Phone: (312) 427-5128

Fax: (312) 427-5139